Stop Overpaying for “Quality” Stocks

Use AI to test quality stocks

“Quality” is one of the most abused words in investing.

Investors use it all the time.

Quality business.

Quality compounder.

Quality franchise.

Sounds smart.

But it’s often useless.

Hermès and a random Polish retailer can both get called "quality"on X.

It’s usually just a premium multiple looking for a justification.

And to justify it, they reach for vague buzzwords.

Like:

Network effects

Economies of scale

Strong brand

It’s easy to call something “quality.”

It’s much harder to explain:

What exactly is better VS the market?

Why should the premuim persist?

And how does it show up in future cash flows?

Because answering those questions takes real work.

That’s where AI helps.

By helping you test whether the premium is real or just a story by checking years of reports, transcripts, and industry history.

In this article, I’ll show you the only 4 reasons a stock deserves a premium multiple and how to test them with AI.

Does this stock really deserve a high multiple?

Buying a stock at 30X earnings can make you more money than buying one at 6x.

But only if that higher multiple is justified by math.

Not by a fancy story around “quality.”

A stock price is just 2 things:

Stock price = earnings × multiple

That’s it.

Now, Imagine 2 stocks, both earns $1.

Stock A trades at 30x.

Stock B trades at 10x.

Same earnings with very different multiple.

Why?

Because the market believes that $1 is more valuable in Stock A.

And that only makes sense if one or more of these is true:

$1 of Stock A earnings will grow much more over time:

If earnings go from $1 today to $3 in a few years, then paying 30x today is the same as paying only 10x those future earnings.

$1 in Stock A will last much longer:

If one business can earn $1 for 20 years and another for only 10 , the first deserves a higher multiple.

Stock A will need less reinvestment to keep growing:

If one business keeps $0.80 of every $1 it earns and another keeps only $0.20, the first deserves a higher multiple.

Stock A’s future cash flows are more reliable:

If one business is very likely to deliver that $1 of earning he deserves a higher multiple.

Let’s break them down.

And see how AI makes each one easier to check.

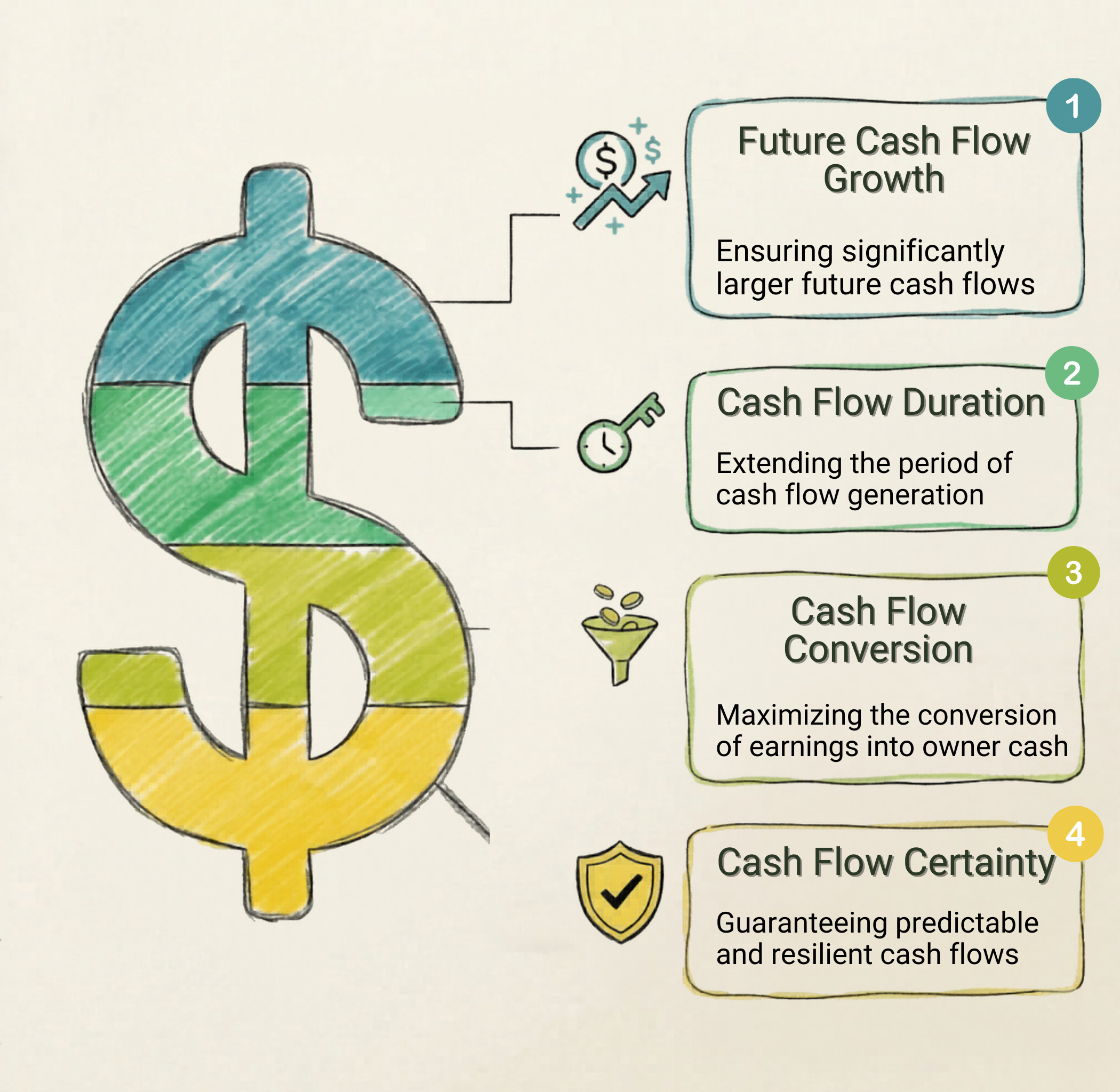

The 4-Part Premium Multiple Test

This framework has 4 buckets.

But each bucket is really a group of questions.

And to answer those questions well, you need 2 things:

Look across multiple years, not just the latest report

Cross-check management claims against numbers and industry evidence

That’s why this is a perfect Deep Research task.

Because the job is not finding one answer.

It’s tracing patterns across years of filings, transcripts, and industry history.

Right now, Gemini is still the best Deep Research tool for this.

(Sorry Claude. You still win on automation of tasks.)

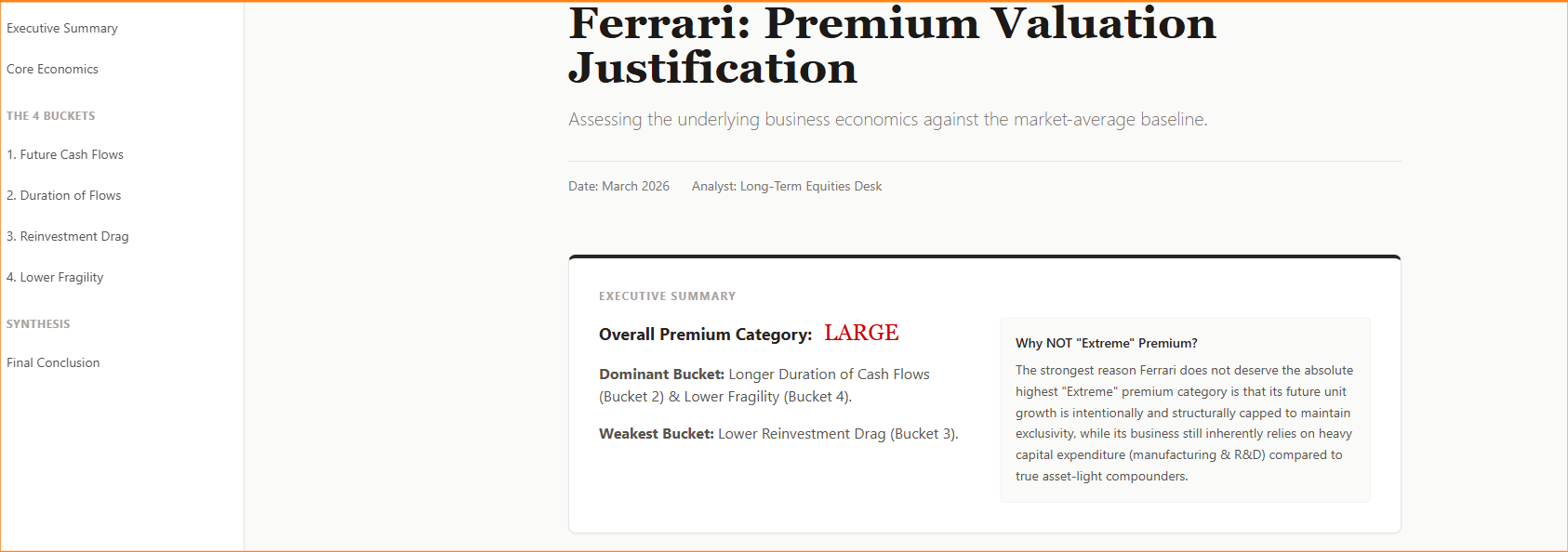

The output: a detailed report and a score for each bucket.

Here’s the exact prompt structure I use to inject real investing logic into Deep Research.

Bucket 1: More Future Owner Cash Flows

Will this business produce materially more owner cash per share over time than a market-average business?

What the prompt checks:

Growth runway: how much room is really left?

Pricing and mix: can higher revenue turn into higher owner earnings?

Operating leverage: does growth actually flow through?

Structural ceiling: what eventually caps the growth?

Bucket 2: Longer Duration of Cash Flows

Will this business sustain strong owner cash flows for much longer than a market-average business?

Duration is not “loyalty.”

It means the cash flows are harder to disrupt, harder to replace, and more painful for customers to walk away from.

What the prompt checks:

Switching costs: what does it really cost to leave?

Mission-criticality: embedded workflow or nice-to-have?

Industry structure: does competition stay rational over time?

Disruption risk: what could make this less relevant in 10 years?

Bucket 3: Lower Reinvestment Drag

Does this business convert earnings into owner cash materially better than a market-average business?

Owner cash is not earnings.

It’s what’s left after the business reinvests what it must to maintain and grow.

Owner Cash = Earnings − Required Maintanance Reinvestment

What the prompt checks:

Capex burden: how much capital is needed just to stay in place?

Working capital: does growth absorb cash as the business scales?

FCF conversion: how much of earnings becomes real cash?

Capital intensity: what must be spent to defend and grow the business?

Bucket 4: Lower Fragility

This is one of the biggest traps..

A strong brand doesn’t automatically mean strong returns.

If that were true, Aston Martin would be a legendary compounder.

It isn’t.

The real question:

Are this company’s future cash flows more reliable than those of a market-average business?

Less fragile means less likely to break in a downturn, disruption, or industry shock.

That can justify a higher multiple.

The prompt To Run

Open Gemini

Use Pro or Thinking mode. Both do a great job

Enable Deep Research

Paste in the prompt bellow