Use AI to Spot Risks You’re Too Biased to Notice

A 3 steps system to copy

AI’s biggest advantage is simple: it’s a machine.

At least for now...

And that one fact gives it an edge no human investor will ever have.

A machine doesn’t get attached to a stock.

It doesn’t fall in love with a CEO.

It doesn’t justify red flags because “the story is still good.”

As investors, we have a tendency to ignore risks until they hit us in the face.

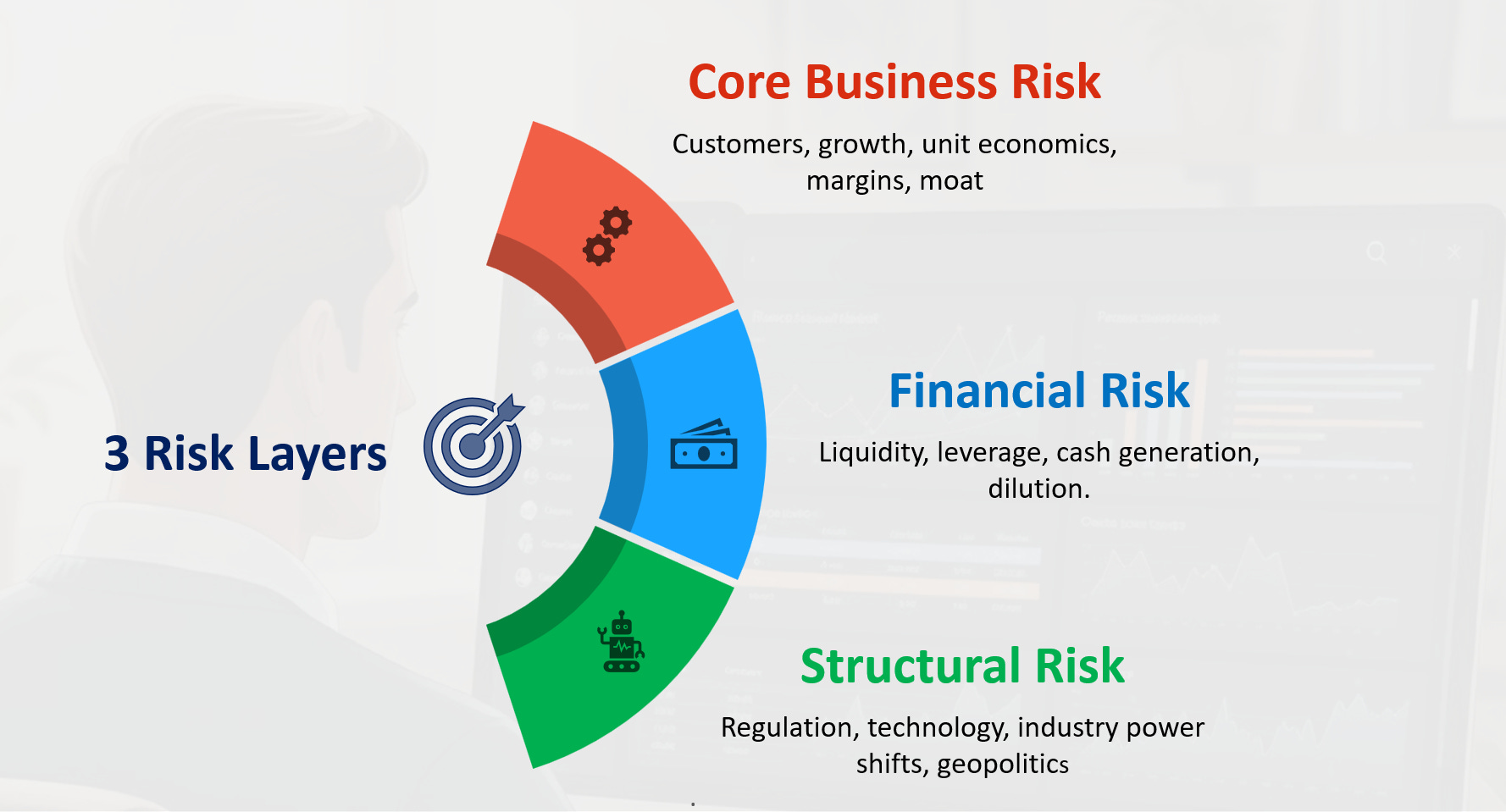

Here’s a 3 layers system to use AI to spot the real business risks before market sees them:

Each layer checks a different angle, and together they give you the full picture of what can break it:

Layer 1 : Inside the business: the operational engine (customers, margins, growth, moat).

Layer 2 : Behind the business: the financial foundation (liquidity, leverage, cash flow).

Layer 3 : Around the business: the external forces (regulation, technology, industry shifts).

Let’s break it down.

Each layer comes with one copy-paste prompt so you can run it immediately.

Layer 1 : Core Business Risk

Layer 1 identify what could break the business from the inside.

It’s about the real mechanics of the business not the accounting.

This step answer one key question:

“Is the business engine truly strong… or already showing early cracks?”

You pressure-test everything that keeps the machine running:

Why customers leave

What slows growth

What compresses margins

Which parts of unit economics are fragile

How the moat could erode

What trends signal early weakness

If you skip this, every other layer loses meaning.

You must understand the engine first.

Prompt Layer 1 (Copy-Paste Ready)

Role:

You are my senior business analyst. Your job is to produce a clear, rigorous, evidence-driven diagnostic of the company’s Core Business Risk (Layer 1).

Company: [insert your stock here]

Mission:

Identify, explain, and quantify the true operational risks that could materially weaken the company’s core engine: moat, customers, revenue drivers, margins, and unit economics.

1. Executive Summary (start with this)

Give a concise, structured summary of the 5–7 highest-impact risks, ranked by severity and likelihood.

Each item = one line: Risk → Why it matters → Evidence indicator.

2. Customer Risk

→ Why could customers leave?

List all realistic reasons and give concrete triggers: price, switching cost, product relevance, quality, alternatives, budget cuts, onboarding friction.

→ Impact on business

Explain how each scenario affects:

revenue

average spend

retention

sales cycles

expansion rate

→ Evidence check

Are there current signs in filings or data that any scenario is starting? (Yes/No + 1 line proof)

3. Growth Risk

→ What could make revenue stop growing?

Analyze barriers: TAM saturation, competitor encroachment, product fatigue, weaker pipelines, sales execution, distribution constraints.

→ Impact quantification

Describe how each factor would hit:

top line

new customer acquisition

pricing power

wallet share

→ Early indicators

Highlight signals the company should monitor.

4. Margin Risk

→ What could make margins decline?

Assess mix shift, pricing pressure, COGS inflation, new product dilution, loss of economies of scale, weaker utilization.

→ Unit economics view

Explain which parts of the model are sensitive and why.

→ Evidence check

Show relevant trailing trends if visible.

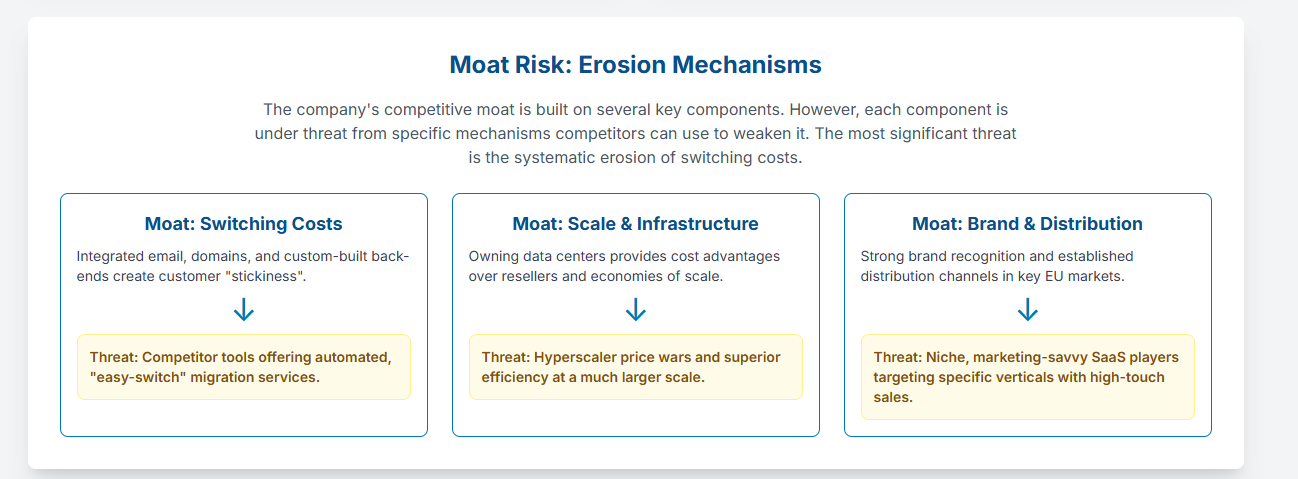

5. Moat Risk

→ What is the moat? Break it down.

Switching costs, brand, network effects, scale, IP, distribution, regulation.

→ What could erode each moat?

Identify mechanisms competitors might use to weaken it.

→ Detect early signs of erosion

Give concrete metrics to track.

6. Final Diagnostic

A table with:

Risk

Severity (High / Medium / Low)

Likelihood (High / Medium / Low)

Evidence today

Management’s ability to mitigateI ran this layer on IONOS Group SE : a European cloud-hosting provider.

It’s the stock I’m digging into right now.

And Layer 1 instantly gave me clarity: where the engine is strong, and where the real business risks live.

Layer 2 :Financial Risk Diagnostic

After checking the engine , the next step is to look behind the business at the financial foundation holding everything together.

Layer 2 asks one question every investor needs answered:

Can this company survive stress… or does one bad cycle break it?

It’s about evaluating proportional, evidence-based financial risks:

Liquidity (cash buffers, short-term safety)

Leverage (net debt vs cash generation)

Debt sustainability (maturities, interest coverage)

Cash flow durability (FCF stability across cycles)

Dilution risk (SBC, share count, capital allocation)

Working-capital behavior (patterns that hide fragility)